จองคิวบริการ

จองคิวบริการ

NR tours

NR tours

NR shop

NR shop

NR jobs

NR jobs

facebook th

facebook th

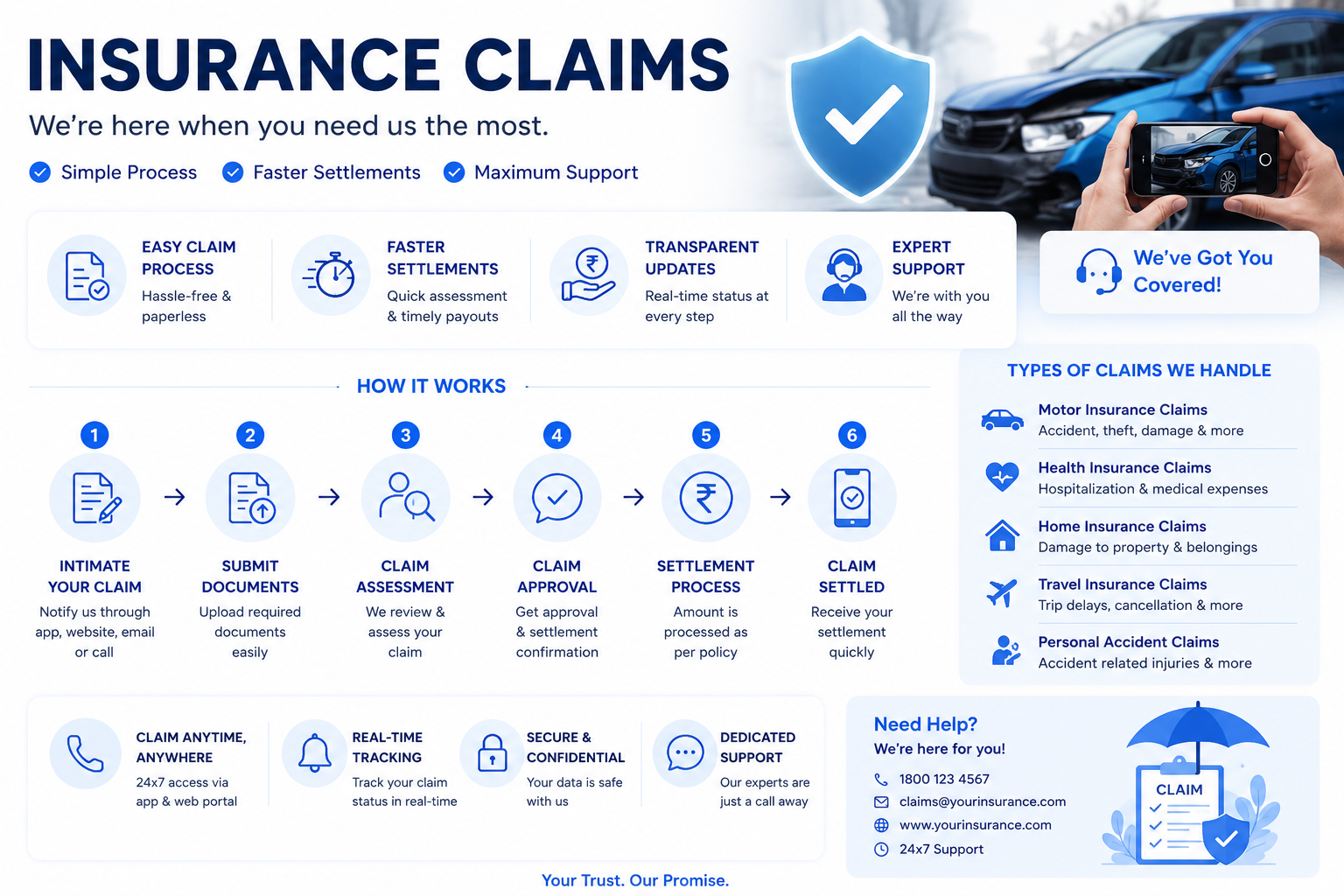

The global landscape for processing policy payouts is undergoing a fundamental shift as legacy systems give way to agile, cloud-based architectures. The Insurance Claims Market is currently defined by an intense focus on reducing cycle times and improving the claimant experience. In an era where financial services are expected to be instantaneous, the ability to manage a loss event with precision and speed has become the ultimate competitive differentiator for carriers worldwide.

Market Overview and Introduction

The core of this sector revolves around the fulfillment of the insurance promise: providing financial restitution when a covered peril occurs. Historically, this was a manual, paper-heavy process prone to delays and human error. However, the introduction of sophisticated claims management software has allowed insurers to centralize data and streamline communication between adjusters, third-party vendors, and policyholders. Furthermore, the rise of insurance claim processing via mobile applications has empowered users to submit photos and documentation immediately after an incident, significantly shortening the traditional "first notice of loss" (FNOL) timeline.

Key Growth Drivers

Several factors are propelling the market forward. First, the increasing frequency of natural disasters is forcing insurers to adopt more robust and scalable processing tools to handle surges in volume. Second, the rise of "InsureTech" startups has introduced a new level of competition, pressuring traditional players to modernize their tech stacks. Additionally, the move toward data-driven underwriting requires a corresponding data-driven claims process, where insights from the settlement phase are fed back into the actuarial models to improve future pricing accuracy.

Consumer Behavior and E-commerce Influence

Today’s consumers are influenced by the seamless experiences provided by retail giants and fintech apps. They no longer tolerate opaque processes or long wait times on phone lines. This "Amazon-ification" of expectations has led to a demand for self-service portals where claimants can track their status in real-time. E-commerce has also introduced new types of risks, such as package theft and shipping damage, creating a niche for high-volume, low-complexity claim handling that must be handled with near-total automation to remain profitable.

Regional Insights and Preferences

North America remains the largest market, characterized by a high adoption of advanced analytics and a complex regulatory environment. In contrast, the Asia-Pacific region is the fastest-growing sector, driven by a burgeoning middle class and a "mobile-first" approach to insurance in countries like India and China. Europe maintains a strong focus on data privacy and consumer protection, influencing the development of "privacy-by-design" claims systems that comply with strict GDPR standards.

Technological Innovations and Emerging Trends

Artificial Intelligence (AI) and Machine Learning (ML) are the primary engines of innovation. Computer vision is now used to analyze damage to vehicles or property from smartphone photos, often providing a repair estimate in seconds. Blockchain technology is being explored for "smart contracts," where a payout is triggered automatically by a verifiable event—such as a flight delay—without the user even needing to file a claim. These "parametric" insurance models represent the future of frictionless settlements.

Sustainability and Eco-friendly Practices

Environmental considerations are beginning to impact the claims world. "Green repairs" are becoming a trend, where insurers encourage the use of recycled parts or sustainable building materials in the restoration process. Additionally, the shift toward paperless, digital-only claims documentation significantly reduces the carbon footprint of the insurance administrative lifecycle. Insurers are also using satellite imagery and drones for remote damage assessment, reducing the need for adjusters to travel long distances via carbon-emitting vehicles.

Challenges, Competition, and Risks

Fraud remains the most persistent challenge, with bad actors using sophisticated digital tools to submit false claims. Insurers must balance the need for speed with rigorous anti-fraud protocols. Competition is also intensifying as non-traditional players, such as auto manufacturers and big-tech firms, begin to offer embedded insurance products that handle the claims process directly within their own ecosystems. Furthermore, the risk of cyberattacks on claims databases poses a significant threat to consumer trust and corporate liability.

Future Outlook and Investment Opportunities

The future of the market lies in "predictive claims management," where IoT sensors in homes and cars alert insurers to a problem before the customer even realizes it. For example, a smart water sensor could detect a leak and trigger a claim and a plumbing repair dispatch simultaneously. Investment opportunities are abundant in startups that specialize in "touchless" processing and those providing specialized tools for the gig economy, where traditional insurance models often fall short.