จองคิวบริการ

จองคิวบริการ

NR tours

NR tours

NR shop

NR shop

NR jobs

NR jobs

facebook th

facebook th

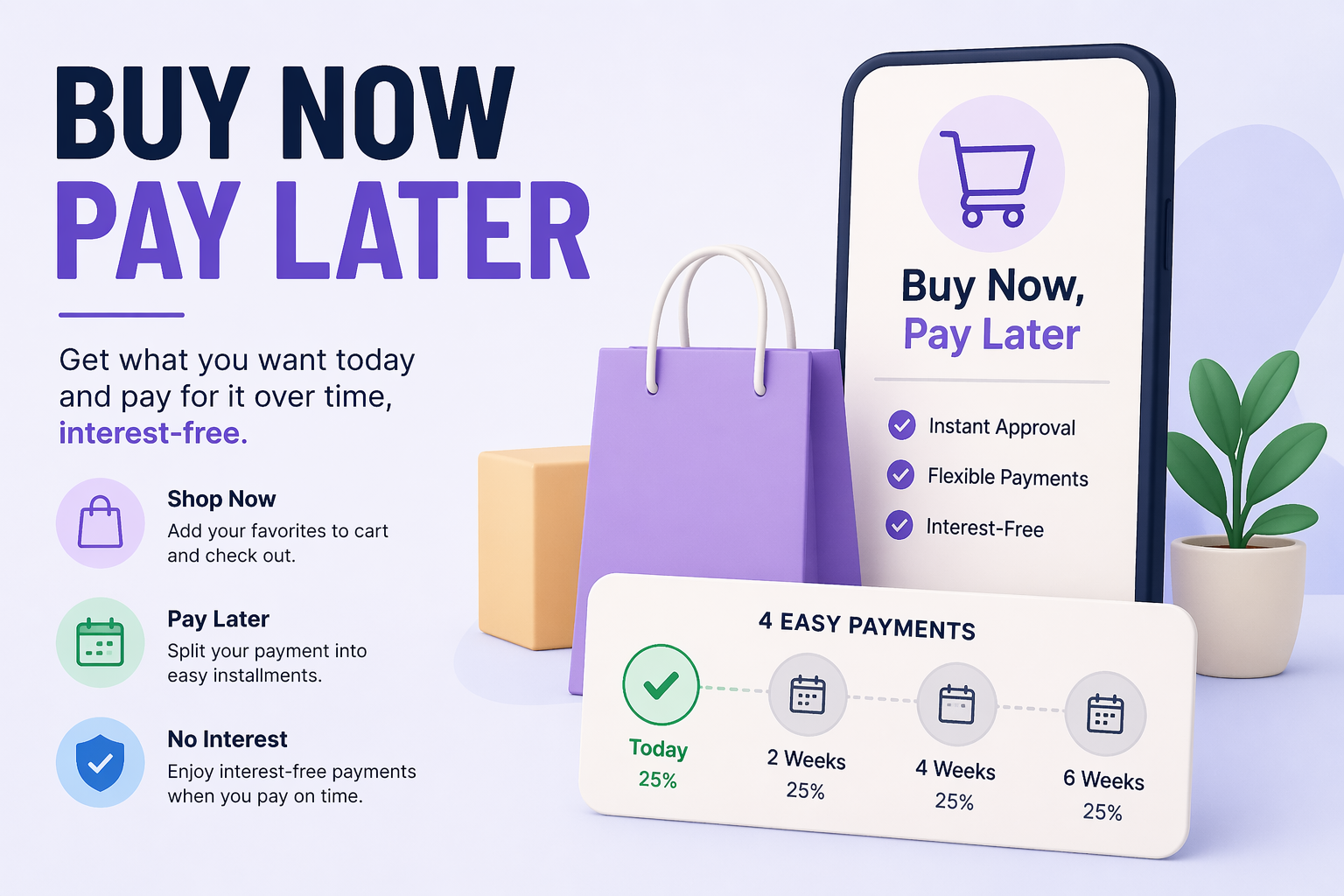

The global Buy Now Pay Later Market has emerged as one of the most disruptive forces in the financial technology sector over the last decade. By providing consumers with the ability to purchase goods immediately while spreading the cost over several interest-free installments, this model has successfully challenged the dominance of traditional credit cards. As digital literacy increases and the demand for transparent financial products grows, BNPL has moved from a niche alternative to a mainstream payment staple. It serves as a bridge between immediate consumer desire and financial responsibility, offering a frictionless checkout experience that benefits both shoppers and merchants.

Market Overview and Introduction

The concept of delayed payment is not new, but the modern execution via BNPL services has transformed the experience through real-time credit checks and seamless app integration. Unlike traditional layaway plans, where the consumer receives the product only after the final payment, BNPL services allow for immediate gratification. This market is characterized by a diverse range of players, from specialized fintech startups to established banking giants and e-commerce platforms. The primary appeal lies in the "interest-free" nature of the core product, typically structured as four bi-weekly payments, which appeals to a generation wary of revolving credit card debt.

Key Growth Drivers

Several factors are propelling this industry forward, most notably the shift in consumer demographics. Millennials and Gen Z shoppers, who often prioritize budgeting and avoid high-interest debt, have found installment payment solutions to be an ideal alternative. These installment payment solutions offer a level of predictability that traditional credit lacks. Furthermore, the rapid expansion of 5G and mobile internet access has made these platforms accessible at the point of sale, whether online or in-store. Merchants are also driving growth, as they see significant increases in average order values (AOV) and a reduction in cart abandonment rates when they offer flexible financing.

Consumer Behavior and E-commerce Influence

The rise of e-commerce is inextricably linked to the success of this payment model. During the global pandemic, online shopping surged, and consumers sought ways to manage their cash flow amidst economic uncertainty. This led to the mass adoption of digital consumer financing. Shoppers now expect flexibility as a standard feature of the checkout process. This behavioral shift has forced even luxury retailers to reconsider their payment strategies, as the ability to break down a high-ticket item into manageable chunks makes premium products accessible to a broader audience.

Regional Insights and Preferences

North America and Europe currently lead the market in terms of transaction volume, with countries like Sweden (the birthplace of Klarna) and Australia (home to Afterpay) serving as early adopters. However, the Asia-Pacific region is poised for the fastest growth. In many emerging markets, credit card penetration remains low, making pay later apps a primary entry point for formal credit. In regions like Southeast Asia and India, the integration of these services into "super-apps" has made them an essential tool for the burgeoning middle class.

Technological Innovations and Emerging Trends

Innovation in the sector is moving toward "Everywhere BNPL." We are seeing the emergence of virtual cards that allow consumers to use these services at any retailer, even those without a direct partnership. Artificial Intelligence and Machine Learning are being utilized to refine underwriting processes, allowing providers to approve more users while minimizing default risks. Furthermore, the integration of these platforms into physical retail through QR codes and NFC technology is bridging the gap between the digital and physical worlds.

Sustainability and Eco-friendly Practices

As consumers become more conscious of their environmental impact, some providers are incorporating sustainability into their business models. This includes features that allow users to track the carbon footprint of their purchases or donate a portion of their payment to environmental causes. By promoting more intentional spending and offering tools for better financial management, these platforms aim to foster a more sustainable relationship between consumers and their consumption habits.

Challenges, Competition, and Risks

Despite its success, the industry faces significant hurdles, primarily in the form of regulatory scrutiny. Governments worldwide are concerned about the potential for consumers to overextend themselves financially. There is a push to classify these services as traditional credit, which would bring stricter reporting requirements. Additionally, as more players enter the space, including tech giants like Apple, competition is driving down the fees that providers can charge merchants, putting pressure on profit margins.

Future Outlook and Investment Opportunities

The future of the sector lies in diversification. We expect to see these providers expand into larger life expenses, such as healthcare, travel, and education. Investment opportunities are abundant for companies that can integrate value-added services, such as personalized marketing and loyalty programs, into their payment platforms. As the market matures, consolidation is likely, with larger financial institutions acquiring smaller fintech players to gain access to their technology and user bases.

Discover Localized Data And Forecasts Across Key Global Regions And Individual Country Markets:

Canada Buy Now Pay Later Market

China Buy Now Pay Later Market

Europe Buy Now Pay Later Market

France Buy Now Pay Later Market

Germany Buy Now Pay Later Market

India Buy Now Pay Later Market

Italy Buy Now Pay Later Market

Japan Buy Now Pay Later Market