จองคิวบริการ

จองคิวบริการ

NR tours

NR tours

NR shop

NR shop

NR jobs

NR jobs

facebook th

facebook th

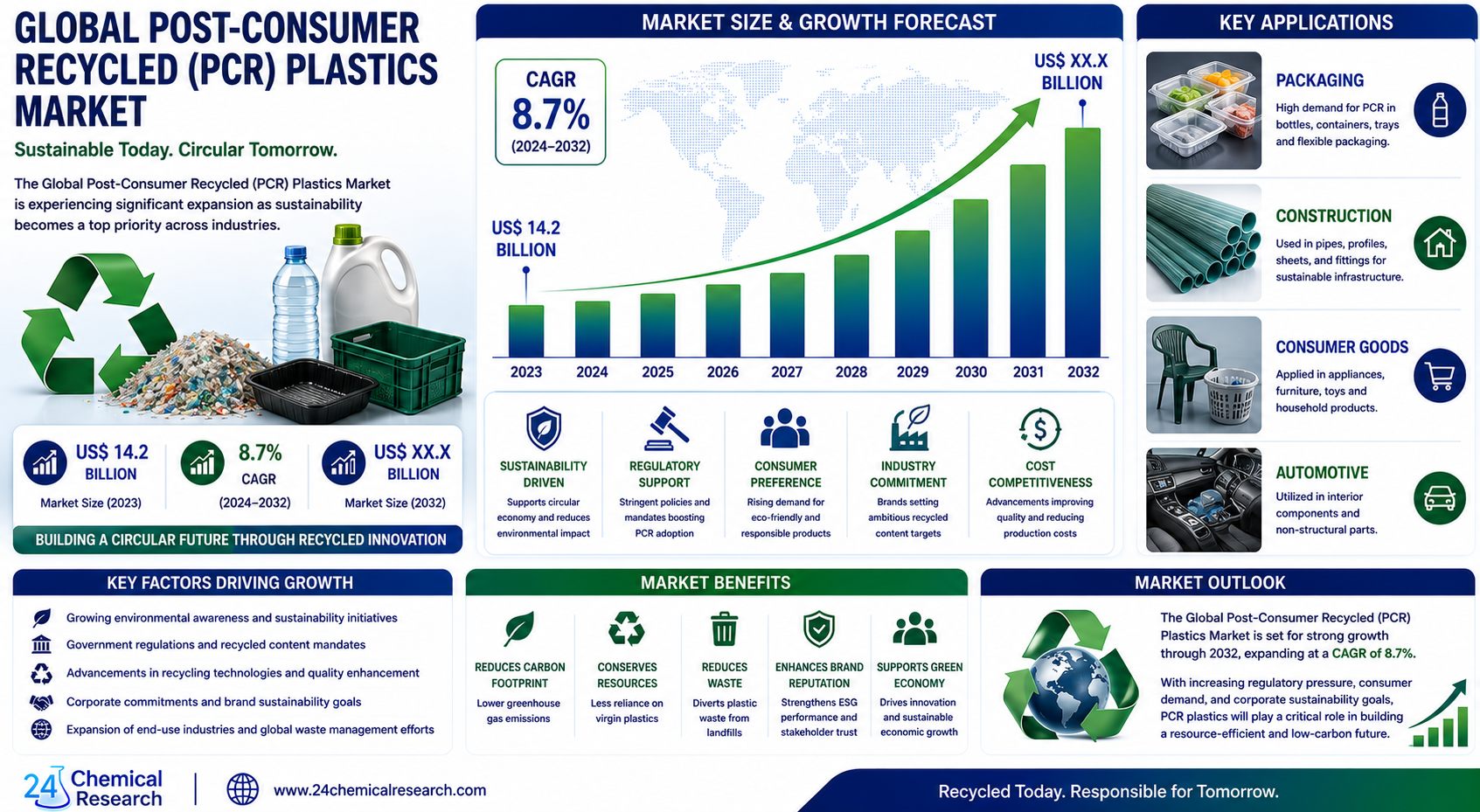

Global Post-Consumer Recycled (PCR) Plastics Market was valued at USD 14.2 billion in 2023 and is projected to expand at a CAGR of 8.7% through 2032. The market's strong growth trajectory is being driven by increasing sustainability commitments, stricter environmental regulations, growing consumer demand for eco-friendly products, and the rapid transition toward circular economy business models across multiple industries.

Post-consumer recycled plastics are materials recovered from household, commercial, and municipal waste streams that are reprocessed into valuable raw materials for manufacturing new products. These recycled polymers play a crucial role in reducing plastic waste, lowering carbon emissions, minimizing landfill dependency, and supporting sustainable resource management.

PCR plastics are increasingly being adopted across packaging, construction, textiles, consumer goods, automotive components, and industrial manufacturing applications. Major multinational brands are accelerating sustainability initiatives, with many committing to incorporate between 30% and 50% recycled content into packaging materials by 2025, creating significant long-term demand for high-quality recycled resins.

Technological advancements in mechanical recycling, chemical recycling, solvent-based purification, artificial intelligence-powered sorting systems, and molecular recycling technologies are further enhancing the performance and quality of PCR materials, enabling their use in increasingly sophisticated applications.

Get Full Report Here:

Download FREE Sample Report:

Market Dynamics

Powerful Market Drivers Propelling Expansion

1. Growing Adoption of Circular Economy Models

The global transition from traditional linear consumption models toward circular economy frameworks remains the primary catalyst for PCR plastics market growth. Governments, corporations, and consumers increasingly prioritize sustainable resource utilization, waste reduction, and recycling initiatives.

Circular economy policies are encouraging manufacturers to incorporate higher levels of recycled content into products, creating substantial demand for PCR plastics across various industries.

2. Rising Sustainability Commitments from Global Brands

Leading companies in packaging, cosmetics, retail, food and beverage, electronics, and consumer goods sectors have announced ambitious sustainability goals requiring significant incorporation of recycled materials.

These commitments are generating long-term demand for recycled PET, recycled polypropylene, recycled polyethylene, and other PCR polymers capable of meeting strict performance and quality standards.

3. Expansion of Sustainable Packaging Applications

Packaging accounts for approximately 62% of total PCR plastics demand, making it the largest application segment globally. Food packaging, beverage containers, personal care packaging, and household product packaging continue driving consumption growth.

The increasing adoption of food-grade recycled PET (rPET) and recycled polypropylene (rPP) is creating significant opportunities throughout the packaging value chain.

4. Government Regulations and Recycled Content Mandates

Regulatory initiatives including Extended Producer Responsibility (EPR) schemes, plastic taxes, recycled content mandates, and waste reduction targets are accelerating adoption of recycled materials.

Many countries are implementing legislation requiring minimum recycled content levels, creating favorable market conditions for PCR plastics manufacturers.

Significant Market Restraints

1. Volatility in Virgin Plastic Pricing

The economics of PCR plastics remain closely linked to virgin resin prices. When crude oil prices decline significantly, virgin plastic materials become more cost-competitive, reducing the financial attractiveness of recycled alternatives.

2. Quality Variability in Recycled Materials

Maintaining consistent quality remains a major challenge for PCR suppliers. Variations in feedstock quality, contamination levels, and processing conditions can affect product performance.

3. Regulatory Fragmentation Across Regions

Different food-contact regulations, certification requirements, and recycling standards across regions complicate international trade and global supply chain integration.

4. Collection Infrastructure Limitations

Many developing economies continue facing challenges related to waste collection, sorting efficiency, and recycling infrastructure, limiting feedstock availability for PCR production.

Critical Market Challenges

One of the most significant challenges facing the PCR plastics industry is achieving consistent material quality while scaling production to meet growing demand. Brand owners increasingly require recycled materials that perform similarly to virgin resins, creating technical challenges for recyclers.

Traceability and certification also remain critical concerns. Companies must demonstrate the authenticity of recycled content claims while complying with evolving sustainability reporting requirements.

The industry additionally faces challenges related to waste collection efficiency, contamination management, and infrastructure investment. Informal waste management systems continue dominating in many regions, creating obstacles to consistent supply chain development.

Global trade restrictions and waste shipment regulations further complicate international recycling flows and raw material sourcing strategies.

Vast Market Opportunities

1. Advanced Chemical Recycling Technologies

Chemical recycling and molecular recycling technologies offer significant opportunities to overcome limitations associated with traditional mechanical recycling. These processes enable conversion of mixed plastic waste into virgin-quality feedstocks.

2. Food-Grade Recycled Packaging

The growing demand for food-contact approved recycled plastics represents one of the most attractive market opportunities. Advanced purification technologies are enabling greater adoption in beverage, food, and healthcare packaging applications.

3. Sustainable Construction Materials

Construction applications are projected to grow at approximately 11.2% CAGR, making this one of the fastest-growing segments. Recycled plastics are increasingly replacing traditional materials in pipes, decking, insulation systems, and building products.

4. Automotive Lightweighting Initiatives

Automotive manufacturers are incorporating PCR materials into vehicle interiors, underbody components, and structural applications as part of broader sustainability and lightweighting strategies.

5. Emerging Applications in Medical and 3D Printing Industries

New opportunities continue emerging in medical device packaging, additive manufacturing, 3D printing filaments, and advanced industrial applications requiring sustainable material solutions.

In-Depth Segment Analysis

By Type

PET (Polyethylene Terephthalate) remains the dominant segment due to its extensive use in beverage bottles, food packaging, textile fibers, and personal care containers. Recycled PET continues benefiting from mature collection systems and strong market acceptance.

PP (Polypropylene) represents one of the fastest-growing categories due to increasing demand in food packaging, automotive components, household products, and consumer goods applications. Advances in purification technologies are expanding its market potential.

HDPE (High-Density Polyethylene) continues seeing strong demand in industrial containers, detergent packaging, pipes, and construction products due to its durability and recyclability.

LDPE (Low-Density Polyethylene) remains important for flexible packaging applications, films, and industrial uses, although recycling challenges continue affecting growth.

Other Polymers including PS, PVC, and specialty plastics represent niche opportunities supported by technological innovation and advanced recycling solutions.

By Application

Packaging remains the largest application segment, accounting for approximately 62% of total market demand. Consumer goods companies increasingly prioritize recycled content to meet sustainability commitments.

Building & Construction is projected to be the fastest-growing application category, supported by infrastructure development and sustainable building initiatives.

Textiles & Apparel continue utilizing recycled plastics for fiber production, performance fabrics, and sustainable fashion products.

Consumer Goods manufacturers increasingly adopt PCR materials in household products, electronics, and personal care packaging.

Industrial Applications and Automotive Components are generating growing demand as companies seek to reduce environmental impact while maintaining product performance.

By End-User Industry

The Packaging Industry remains the largest consumer of PCR plastics due to aggressive sustainability goals and regulatory requirements.

Construction companies increasingly adopt recycled materials in infrastructure projects and building products.

Textile manufacturers continue incorporating recycled PET fibers into apparel and industrial fabrics.

Automotive manufacturers utilize PCR plastics to improve vehicle sustainability and reduce carbon footprints.

Consumer goods producers, industrial manufacturers, and electronics companies further contribute to market expansion.

Competitive Landscape

Market Segmentation and Key Players

Veolia Polymers

Indorama Ventures

ALPLA Werke

KW Plastics

B&B Plastics

Clear Path Recycling

JS Plastics

PolyQuest

UltrePET

Envision Plastics

Phoenix Technologies

Far Eastern New Century

Kyoei Industry

Shazil Pakistan

Shandong Power Environmental

The global PCR plastics market is highly competitive, featuring waste management companies, recycling specialists, polymer producers, and integrated packaging manufacturers. Competition centers on feedstock access, recycling technology capabilities, product quality, certification standards, and sustainability credentials.

Leading market participants continue investing heavily in recycling infrastructure, chemical recycling technologies, advanced sorting systems, and food-grade recycling capabilities. Strategic partnerships between recyclers, packaging manufacturers, brand owners, and waste collection organizations are becoming increasingly important.

Innovation in AI-based sorting systems, solvent purification technologies, and molecular recycling platforms continues shaping the industry's competitive landscape.

Regional Analysis

Europe

Europe leads the global PCR plastics market with approximately 42% market share. Strong regulatory frameworks including EPR schemes and the Single-Use Plastics Directive continue driving adoption of recycled materials.

Germany, France, and Scandinavian countries remain leaders in recycling innovation, deposit return systems, and closed-loop material management.

North America

North America is experiencing rapid growth due to corporate sustainability commitments and state-level recycled content mandates. California and New York continue driving demand through progressive environmental policies.

Investments in food-grade rPET facilities and advanced recycling technologies further support regional growth.

Asia-Pacific

Asia-Pacific presents substantial growth opportunities despite infrastructure challenges. China remains a major market due to its large manufacturing base, while Japan maintains one of the world's highest plastic recycling rates at approximately 85%.

India, Indonesia, Vietnam, and other emerging economies continue investing in formalized waste collection and recycling networks.

Latin America

Latin America is gradually expanding its recycling infrastructure, supported by government initiatives, multinational corporate investments, and increasing environmental awareness.

Middle East & Africa

The Middle East and Africa region is witnessing growing adoption of sustainable packaging and recycling technologies as governments implement waste reduction strategies and circular economy programs.

Frequently Asked Questions (FAQs)

1. What are Post-Consumer Recycled (PCR) Plastics?

Post-consumer recycled plastics are materials recovered from household, commercial, and municipal waste streams that are processed and reused as raw materials for manufacturing new products.

2. What is driving growth in the PCR plastics market?

Growth is primarily driven by sustainability regulations, circular economy initiatives, recycled content mandates, corporate environmental commitments, and increasing consumer demand for eco-friendly products.

3. Which industries use PCR plastics?

Major end-user industries include packaging, construction, textiles, automotive, consumer goods, industrial manufacturing, and electronics sectors.

4. What are the major applications of PCR plastics?

Key applications include rigid and flexible packaging, construction materials, textile fibers, automotive components, consumer products, industrial equipment, and sustainable manufacturing solutions.

5. Which region dominates the PCR plastics market?

Europe currently leads the global market with approximately 42% market share, supported by strong environmental regulations, advanced recycling infrastructure, and aggressive circular economy policies.

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch