จองคิวบริการ

จองคิวบริการ

NR tours

NR tours

NR shop

NR shop

NR jobs

NR jobs

facebook th

facebook th

When durability, chemical resistance, and long-term surface protection are non-negotiable requirements, fluorocarbon coatings consistently rank among the most trusted solutions available to engineers and specifiers. The Fluorocarbon Coating Market is projected to grow from US$ 826.42 Million in 2025 to US$ 1,256.84 Million by 2034, recording a CAGR of 5.38% over the 2026 to 2034 forecast period. Driven by sustained demand from architecture, electronics, aerospace, and industrial machinery sectors, this market is expanding steadily as end users prioritise long-life coatings that reduce maintenance costs and extend asset service life.

What Are Fluorocarbon Coatings?

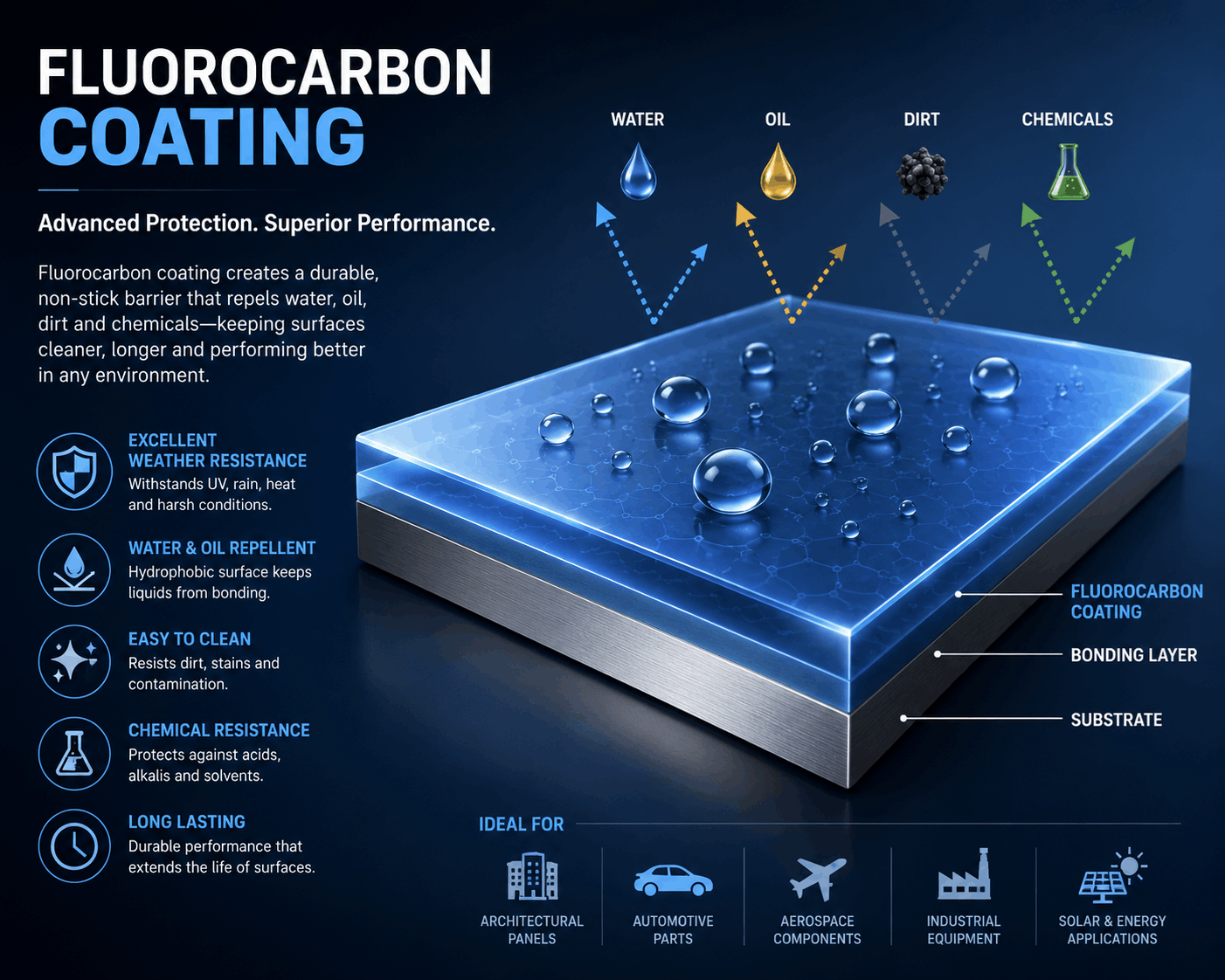

Fluorocarbon coatings are high-performance surface treatments based on fluoropolymer chemistries, including PTFE, PVDF, FEP, and FEVE, applied to substrates to impart exceptional resistance to corrosion, UV degradation, heat, chemicals, and surface friction. Their unique carbon-fluorine bond structure delivers hydrophobic, non-stick, and weathering-resistant properties that far exceed those of conventional organic coatings. Available in solvent-borne and waterborne technology platforms, they are applied across metals, glass, plastics, and composite substrates in both industrial and decorative contexts.

Request a Sample Copy of the Report: https://www.theinsightpartners.com/sample/TIPRE00025509

Key Market Players

- AGC Chemicals

- DAIKIN INDUSTRIES, Ltd.

- Fluorocarbon Surface Technologies

- Arkema

- Solvay

- Blinex Filter-Coat Pvt. Ltd.

- The Chemours Company

- Akzo Nobel N.V.

- Honeywell International Inc.

- Kansai Paint Co., Ltd.

What Is Driving Growth in the Fluorocarbon Coating Market?

Architectural applications are the largest and most consistent demand driver. PVDF and FEVE-based fluorocarbon coatings are widely specified for aluminium cladding, curtain wall systems, window frames, and roofing elements on commercial and high-rise buildings. Their ability to retain colour and gloss for decades without significant chalking, fading, or corrosion makes them the premium choice for landmark buildings and high-specification construction projects. Rapid urbanisation across Asia Pacific, combined with infrastructure investment in the Middle East and North America, is generating substantial demand for high-performance architectural coatings that deliver long service life with minimal maintenance intervention.

The electronics industry provides a growing and technically demanding demand channel. Fluorocarbon coatings are applied to printed circuit boards, semiconductors, connectors, and electronic enclosures to protect against moisture ingress, chemical contamination, and thermal stress. As electronic devices become smaller, more powerful, and deployed in harsher environments, the need for reliable conformal and protective coatings intensifies. The rapid expansion of electric vehicle power electronics, industrial automation equipment, and consumer wearables is pulling through increased volumes of fluorocarbon coating consumption in this segment.

Aerospace applications represent a high-value demand stream where fluorocarbon coatings earn a premium for their performance in extreme conditions. PTFE and FEP coatings are used on fasteners, actuator components, fuel system parts, and airframe elements to reduce friction, prevent corrosion, and maintain dimensional stability across wide temperature ranges. With commercial aviation fleet sizes continuing to grow globally and defence aviation programmes accelerating in multiple regions, aerospace-grade fluorocarbon coating demand is on a firm upward trajectory.

Industrial machinery and equipment completes the picture. Fluorocarbon coatings on process vessels, pumps, valves, heat exchangers, and conveyor components reduce wear, prevent chemical attack, and lower cleaning frequency in food processing, chemical manufacturing, and pharmaceutical production environments. The total cost of ownership argument is compelling for plant operators, as extended maintenance intervals and reduced downtime more than offset the premium cost of fluorocarbon-coated components over conventionally coated alternatives.

Segmentation Overview

The Fluorocarbon Coating Market is segmented as follows:

By Technology:

- Solvent-Borne

- Waterborne

By Type:

- Polytetrafluoroethylene (PTFE)

- Polyvinylidene Difluoride (PVDF)

- Fluorinatedethylenepropylene (FEP)

- Fluoroethylene (FEVE)

- Others

By Application:

- Architecture

- Electronics

- Machinery Industry

- Aerospace

- Others

Sustainability and Innovation Trends

The fluorocarbon coatings industry is navigating a significant sustainability transition driven by regulatory scrutiny of PFAS compounds. While the fluoropolymers used in most fluorocarbon coatings are distinct from the short-chain PFAS substances subject to the most stringent restrictions, the broader regulatory environment has prompted manufacturers to invest in cleaner production processes and lower-fluorine-content alternatives for applications where the full performance spectrum of traditional fluorocarbon coatings is not required.

Waterborne fluorocarbon coating technology is the most commercially significant innovation response to sustainability pressure. Transitioning from solvent-borne to waterborne platforms reduces VOC emissions during application, improving compliance with air quality regulations in the EU, North America, and increasingly in China. Several leading producers have invested substantially in waterborne PVDF and FEVE formulation development, achieving performance parity with solvent-borne systems in architectural and general industrial applications, and driving accelerating adoption in regulated markets.

Buy Premium Report: https://www.theinsightpartners.com/buy/TIPRE00025509

Regional Outlook

Asia Pacific is the largest and fastest-growing regional market, anchored by China's massive construction sector, its dominant electronics manufacturing base, and the presence of significant fluorochemical production capacity in Japan and China. DAIKIN, AGC, and Kansai Paint's strong regional positions reflect the depth of fluorocarbon coating demand across the region. North America maintains strong demand through aerospace, industrial, and commercial construction segments, with The Chemours Company providing a robust domestic supply foundation. Europe shows consistent demand driven by premium architectural projects, stringent industrial coating standards, and the regulatory environment encouraging waterborne technology adoption. South and Central America represent a developing opportunity tied to construction and industrial sector growth across Brazil and Mexico.

Related Reports:

Anti-Reflective Coatings Market

MRO Protective Coatings Market

About The Insight Partners

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

Contact Us:

If you have any queries about this report or if you would like further information, please contact us:

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available in: Korean | German | Japanese | French | Chinese | Italian | Spanish