จองคิวบริการ

จองคิวบริการ

NR tours

NR tours

NR shop

NR shop

NR jobs

NR jobs

facebook th

facebook th

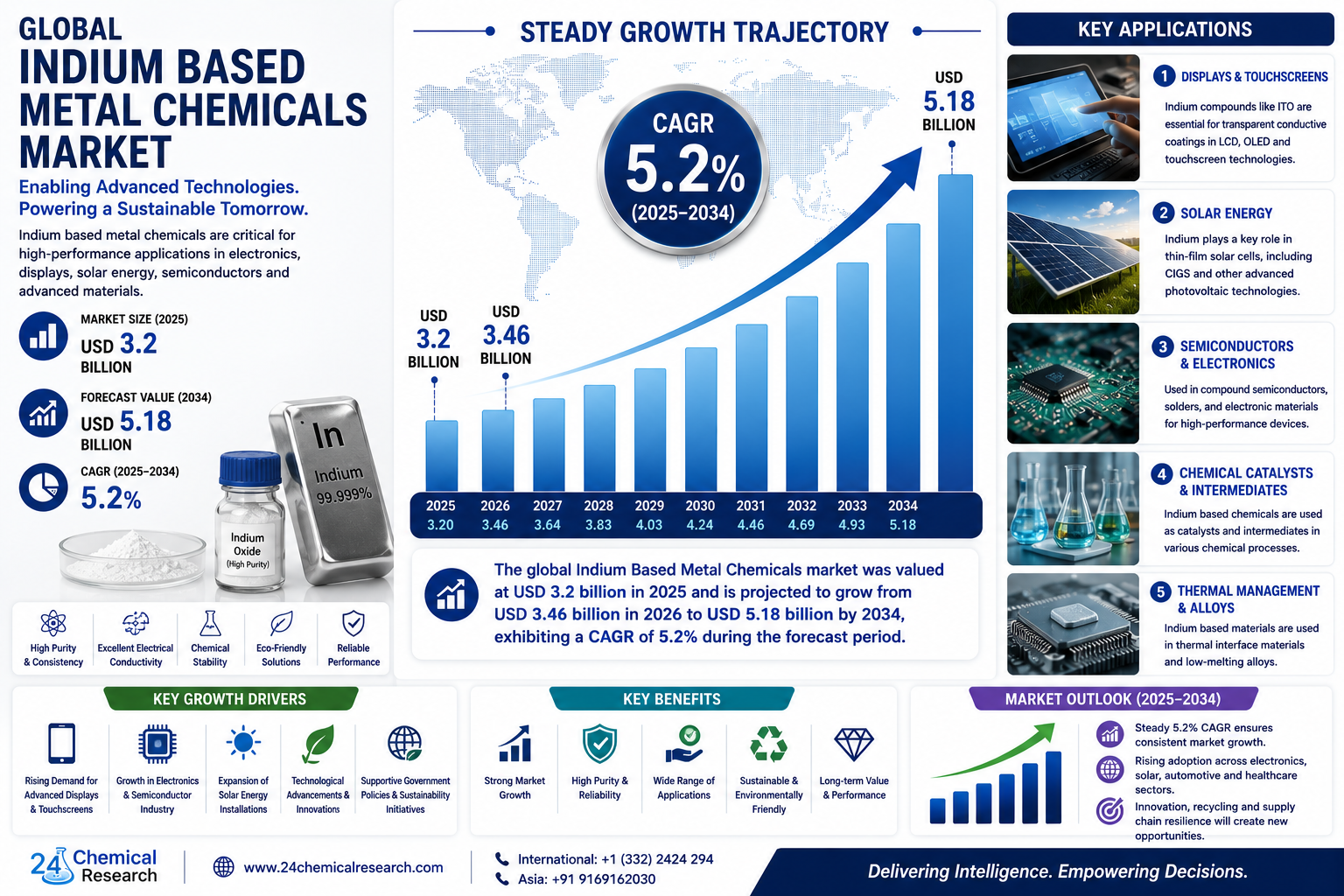

Indium based metal chemicals represent a specialized class of advanced materials derived from indium, a rare post-transition metal that is recovered mainly as a byproduct of zinc smelting operations. Although indium is used in relatively small volumes compared with major industrial metals, its chemical compounds are strategically important because they support high-performance electronics, display technologies, semiconductors, optoelectronics, and thin-film energy applications.

What makes indium based metal chemicals valuable is their rare combination of properties. These materials offer high electrical conductivity, strong optical transparency in thin-film form, low melting points, and excellent compatibility with semiconductor manufacturing processes. These characteristics are difficult to replicate with many alternative materials, which is why indium compounds remain critical in several advanced technology supply chains.

The most commercially significant compound in this family is Indium Tin Oxide, commonly known as ITO. ITO is widely used as a transparent conductive film in flat panel displays, touch panels, LCDs, OLED panels, and other screen-based devices. Beyond ITO, the market includes Indium Phosphide (InP) for high-speed photonic and semiconductor applications, Indium Antimonide (InSb) for infrared detection, and Indium Gallium Zinc Oxide (IGZO) for next-generation display backplanes. Supporting compounds such as Indium Oxide, Indium Chloride, and Indium Sulfide also serve specialized roles in electronics manufacturing and advanced materials development.

The Indium Based Metal Chemicals market is experiencing consistent, measured growth, driven by long-term demand from consumer electronics, semiconductors, thin-film photovoltaics, advanced displays, and optoelectronic devices. However, this growth exists alongside real supply complexity. Indium prices are volatile because supply is linked to zinc refining output rather than direct primary mining. As a result, producers and end-users are increasingly focusing on supply security, advanced purification, recycling, and strategic partnerships.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307153/indium-based-metal-chemicals-market

Market Dynamics:

The Indium Based Metal Chemicals market is shaped by a complex interplay of powerful growth drivers, supply chain constraints, technical challenges, substitution risks, and emerging opportunities in advanced displays, semiconductors, quantum technologies, circular economy systems, and renewable energy applications.

Key Market Highlights

● Indium Tin Oxide accounts for approximately 70% of total indium consumption, mainly through transparent conductive coatings used in LCDs, OLED panels, and touchscreens.

● Electronics and display manufacturing remain the largest demand centers for indium based metal chemicals.

● Indium Phosphide is gaining strong traction in photonic integrated circuits, data center optical interconnects, 5G infrastructure, and high-speed semiconductor applications.

● CIGS thin-film solar cells are creating new demand for high-purity indium compounds in renewable energy technologies.

● Asia-Pacific dominates the market, holding approximately 68% of global share, led by China, Japan, and South Korea.

● IGZO is emerging as a high-value growth segment due to its role in advanced display backplanes and low-power high-resolution screens.

● Recycling infrastructure and secondary indium recovery are becoming critical for improving supply chain resilience and reducing price volatility.

Powerful Market Drivers Propelling Expansion

-

Surging Demand from the Global Electronics and Display Industry:

The largest driver of the Indium Based Metal Chemicals market is the continued expansion of consumer electronics and advanced display technologies. Indium Tin Oxide remains one of the most important materials in this space because it provides both electrical conductivity and optical transparency.

ITO is used as a transparent conductive coating in LCDs, OLED panels, touchscreens, tablets, smartphones, televisions, monitors, wearable devices, and industrial display systems. These applications require thin conductive films that allow light to pass through while enabling touch response and electrical functionality.

Indium Tin Oxide accounts for approximately 70% of total indium consumption, making display technology the dominant demand channel for indium based metal chemicals. With global display production growing at 6–8% annually, the electronics sector continues to provide a strong foundation for market expansion.

Every new generation of smartphones, tablets, laptops, smart displays, and large-format televisions increases demand for higher-quality ITO sputtering targets and high-purity indium chemicals. As devices become thinner, lighter, more energy-efficient, and more responsive, material purity and film performance become increasingly important.

The global electronics market, valued at more than $1.5 trillion, continues to push manufacturers toward improved conductivity, transparency, miniaturization, and manufacturing efficiency. Indium-based materials remain central to this transition.

-

Expansion of the Semiconductor and Optoelectronics Sector:

Beyond displays, the semiconductor and optoelectronics industries are creating a rapidly growing second pillar of demand for indium based metal chemicals. Indium Phosphide is one of the most important compounds in this segment because of its strong electron mobility, direct bandgap properties, and suitability for high-speed and light-based technologies.

InP wafers are used in photonic integrated circuits, high-frequency wireless components, laser diodes, photodetectors, fiber-optic communication systems, and data center optical interconnects. These applications are expanding as global demand for faster data transmission, cloud computing, artificial intelligence infrastructure, and 5G communication networks increases.

Recent growth in LED technology and optoelectronics has also supported stronger consumption of indium phosphide. InP-based materials are valuable because they can handle high-frequency and optical signal applications where traditional silicon materials may face performance limitations.

The global rollout of 5G infrastructure is further increasing demand for indium-based alloys and compounds used in high-frequency components, advanced semiconductors, and thermal interface materials. These applications require high-performance materials that can operate reliably under demanding electrical and thermal conditions.

As semiconductor manufacturing becomes more specialized, demand for high-purity indium chemicals is expected to strengthen across photonics, RF components, infrared detection, advanced sensing, and next-generation computing applications.

-

Rising Adoption of Thin-Film Photovoltaics and Renewable Energy Technologies:

The global energy transition is creating a meaningful new demand channel for the Indium Based Metal Chemicals market. Copper Indium Gallium Selenide, commonly known as CIGS, is one of the most important thin-film solar technologies that uses indium compounds.

CIGS solar cells are valued for their flexibility, lightweight construction, low-light performance, and potential use in building-integrated photovoltaics, portable solar devices, flexible panels, and specialty renewable energy systems. While silicon photovoltaics dominate the overall solar market, CIGS remains attractive for applications where design flexibility and weight reduction are important.

The solar energy sector has been expanding at a compound annual growth rate of 9–11% in recent years, supported by government incentives, renewable energy targets, carbon reduction policies, and increasing investment in clean energy infrastructure.

CIGS-based solar modules currently represent a smaller share of the overall photovoltaics market, but they are a high-value application that requires high-purity indium compounds. This creates attractive opportunities for producers capable of supplying consistent, application-specific indium materials.

As renewable energy deployment continues across Europe, Asia, North America, and emerging markets, indium’s role in thin-film solar technologies may become increasingly important.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307153/indium-based-metal-chemicals-market

Significant Market Restraints Challenging Adoption

Despite its strong demand outlook, the Indium Based Metal Chemicals market faces persistent restraints that require careful management by producers, refiners, electronics manufacturers, and semiconductor companies.

-

Supply Chain Vulnerabilities and Indium Scarcity:

The most structurally challenging aspect of the market is the constrained nature of indium supply. Global primary indium production stands at approximately 1,000 metric tons annually, and the metal is recovered mainly as a byproduct of zinc refining rather than mined directly.

This means indium supply depends on zinc production decisions made by smelters around the world. If zinc output slows due to environmental regulations, ore depletion, weak pricing, energy costs, or economic cycles, indium availability can contract even when demand remains strong.

China controls over 50% of global refined indium output, creating significant geopolitical concentration risk. Export policies, domestic industrial priorities, trade restrictions, or regulatory changes in China can affect global availability and pricing.

Price volatility is a direct result of this supply structure. Indium prices can swing by 20–30% annually, making long-term procurement planning difficult for display manufacturers, semiconductor companies, and electronics suppliers.

For companies considering new indium-intensive technologies, supply uncertainty can create hesitation. Stable access to indium chemicals is essential for manufacturers that require consistent material quality and predictable costs.

-

Regulatory Compliance and Environmental Pressures:

The regulatory environment surrounding metal chemicals is becoming stricter, especially in Europe, North America, and advanced Asian markets. Indium compounds are subject to controls related to worker safety, chemical handling, waste management, and environmental exposure.

In Europe, REACH and RoHS directives impose strict requirements on the use, handling, and documentation of indium compounds in manufacturing. Compliance can add 15–20% to production costs for indium chemical producers due to testing, reporting, safety controls, and additional processing requirements.

Although indium is not generally classified as acutely toxic in the same way as some heavy metals, occupational safety concerns have increased, especially for fine indium powder. Documented cases of indium lung disease in workers have led to stricter respiratory exposure limits and workplace safety standards.

Meeting these standards requires investment in ventilation systems, containment equipment, personal protective equipment, monitoring systems, and worker training. These costs can be especially challenging for smaller producers with limited capital resources.

Critical Market Challenges Requiring Innovation

The transition from niche specialty chemical use to broader industrial-scale application creates several challenges for the Indium Based Metal Chemicals market.

One major technical challenge is material substitution, especially in flexible display applications. ITO has long been the default transparent conductor for displays, but its brittleness becomes a limitation in foldable, rollable, and flexible display formats.

Alternative transparent conductors such as silver nanowires, graphene-based films, carbon nanotubes, conductive polymers, and metal mesh technologies are making technical progress. While none has fully replaced ITO’s combination of conductivity, transparency, process maturity, and established manufacturing infrastructure, the competitive pressure is real.

The market also faces the challenge of high-purity processing economics. Semiconductor and display applications increasingly require indium compounds with impurity levels measured in parts per billion. Producing these materials requires multi-stage refining, controlled environments, advanced analytical testing, and rigorous quality systems.

Achieving consistent purity above 99.99% at commercial scale is capital-intensive and technically demanding. Market leaders are investing 8–12% of revenue in purification research and development to maintain their competitive edge.

Supplier qualification is another important barrier. In semiconductor applications, qualifying a new indium chemical supplier can take 6–18 months because customers must validate material performance, purity, consistency, and reliability. This reinforces long-term relationships between established suppliers and major end-users, while limiting disruption from newer producers.

Vast Market Opportunities on the Horizon

-

Next-Generation Display Technologies and IGZO Adoption:

Indium Gallium Zinc Oxide is one of the most important emerging opportunities in the Indium Based Metal Chemicals market. While ITO remains the workhorse of the display industry, IGZO is gaining strong attention as a thin-film transistor material for next-generation displays.

IGZO offers higher electron mobility compared to conventional amorphous silicon. This allows faster response times, improved energy efficiency, better pixel control, and support for high-resolution displays. These advantages are valuable in smartphones, tablets, premium monitors, OLED displays, ultra-high-definition screens, and low-power devices.

Leading display manufacturers in Japan, South Korea, and China are actively transitioning advanced production lines toward IGZO backplane technology. This shift does not reduce indium demand. Instead, it diversifies and elevates demand because IGZO requires precisely formulated multi-component indium compounds.

As display makers pursue higher resolution, thinner panels, lower power consumption, and better screen performance, demand for IGZO and related indium-based materials is expected to grow.

-

Quantum Computing and Advanced Photonics:

Advanced photonics and quantum technologies represent a high-value frontier for indium based metal chemicals. Indium-based compound semiconductors, particularly Indium Phosphide, are gaining attention for quantum dot applications, photonic components, and quantum computing architectures.

InP offers strong bandgap engineering properties and compatibility with light-based signal transmission. These qualities make it valuable for photonic integrated circuits, quantum communication systems, optical computing research, and advanced data transmission technologies.

The quantum technology sector is projected to grow at a CAGR exceeding 25% over the coming decade. While large-scale commercial adoption remains early, specialized materials used in quantum and photonic systems can command premium pricing.

Companies with established high-purity production infrastructure are well positioned to serve this demand as quantum computing, photonic chips, and advanced optoelectronic systems move closer to commercialization.

-

Circular Economy and Recycling Infrastructure Development:

Recycling represents one of the most important strategic opportunities in the Indium Based Metal Chemicals market. Current global indium recycling rates remain below 30%, even though large quantities of indium are used in ITO sputtering targets, display panels, and electronic devices.

Improved recovery infrastructure from end-of-life electronics and manufacturing scrap could significantly improve supply security. New hydrometallurgical recovery processes are being developed to recover indium from ITO manufacturing scrap, LCD panels, and end-of-life display systems.

Companies such as Umicore are advancing recycling technologies that can achieve indium recovery rates above 85% from selected waste streams. This could reduce dependence on primary zinc-related indium supply and help moderate price volatility.

Recycling also supports circular economy regulations in Europe and Asia. As governments and manufacturers focus more strongly on resource efficiency, waste reduction, and critical material recovery, secondary indium supply is expected to become increasingly important.

This is not only a sustainability opportunity. It is also a supply chain resilience strategy for electronics, display, and semiconductor industries that depend on stable indium availability.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The indium based metal chemicals market is segmented into:

● Indium Tin Oxide (ITO)

● Indium Phosphide (InP)

● Indium Antimonide (InSb)

● Indium Gallium Zinc Oxide (IGZO)

● Indium Hydroxide

● Other specialty compounds

Indium Tin Oxide currently dominates the market by a substantial margin. Its established role in transparent conductive films for displays and touch panels has made it the default material for the display industry over several decades. Its compatibility with physical vapor deposition and high-volume manufacturing lines supports continued demand.

Indium Gallium Zinc Oxide is attracting strong strategic attention. IGZO is increasingly used in advanced display backplanes because it supports higher resolution, faster response times, and lower power consumption. As premium display technologies grow, demand for IGZO-grade indium compounds is expected to increase.

Indium Phosphide is smaller in volume but growing rapidly. It commands a significant price premium because of its use in compound semiconductors, photonic devices, 5G components, laser diodes, and optical communication systems.

Indium Antimonide serves specialized applications in infrared detection, night-vision systems, aerospace sensors, and defense-related optoelectronics. Indium Hydroxide and other specialty compounds support chemical synthesis, semiconductor processing, coatings, and research applications.

By Application:

Application segments include:

● ITO Manufacturing

● Semiconductor Production

● Solder and Alloys

● Photovoltaic Cells

● Others

ITO Manufacturing remains the dominant application by volume. Global display production creates steady demand for ITO sputtering targets and transparent conductive coatings used in LCDs, OLEDs, touchscreens, and flat-panel displays.

Semiconductor Production is showing the most compelling growth trajectory. This segment includes InP-based photonic devices, compound semiconductors for 5G, optoelectronics, quantum technologies, and high-frequency components. These applications require high-purity and application-specific indium compounds.

Photovoltaic Cells are gaining momentum as CIGS technology matures. Although CIGS remains smaller than silicon photovoltaics, it offers advantages in flexibility, lightweight design, and low-light performance. This makes it attractive for specialty solar applications.

Solder and Alloy applications provide a stable baseline of demand. Indium-containing alloys are used in low-melting-point solders, thermal interface materials, electronic assembly, and industrial bonding applications.

Other applications include infrared detection, sensors, advanced coatings, smart glass, research materials, and specialty chemical processing.

By End-User Industry:

The end-user landscape includes:

● Electronics Manufacturers

● Automotive Industry

● Energy Sector

● Research Institutions

Electronics Manufacturers form the core consumer base for indium based metal chemicals. Display panels, touchscreens, semiconductors, sensors, LEDs, optical components, and electronic assemblies account for the majority of demand.

The Automotive Industry is becoming an increasingly important growth segment. Modern vehicles use smart glass, heads-up displays, infotainment screens, advanced sensors, driver assistance systems, thermal materials, and electronic control systems. These technologies increase demand for ITO, IGZO, InP, and related indium compounds.

The Energy Sector represents a promising long-term opportunity through thin-film photovoltaics, especially CIGS solar cells. As renewable energy adoption grows, demand for high-purity indium compounds in flexible and specialty solar technologies may expand.

Research Institutions play a smaller role in volume terms but are highly important for innovation. Universities, laboratories, and corporate R&D centers use indium compounds in quantum computing, photonics, semiconductor development, advanced display materials, and next-generation optoelectronics.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307153/indium-based-metal-chemicals-market

Frequently Asked Questions

What are indium based metal chemicals used for?

Indium based metal chemicals are used in ITO coatings, touchscreens, LCDs, OLED panels, compound semiconductors, infrared detectors, IGZO display backplanes, CIGS solar cells, solder alloys, thermal interface materials, and advanced photonics. Their conductivity, optical transparency, and semiconductor compatibility make them critical for high-tech applications.

What is driving the Indium Based Metal Chemicals market?

The market is driven by rising demand from consumer electronics, display technologies, semiconductors, 5G infrastructure, photonics, thin-film photovoltaics, and advanced automotive electronics. ITO manufacturing remains the largest demand source, while IGZO, InP, and CIGS applications are creating new high-value growth opportunities.

Which compound dominates the Indium Based Metal Chemicals market?

Indium Tin Oxide dominates the market because it is widely used as a transparent conductive coating in LCDs, OLED panels, touchscreens, and flat-panel displays. Its strong combination of transparency, conductivity, and manufacturing compatibility has made it the leading indium-based compound.

Why is indium supply vulnerable?

Indium supply is vulnerable because it is recovered mainly as a byproduct of zinc refining rather than mined directly. Its availability depends on zinc production decisions, and China controls over 50% of global refined indium output. This creates supply concentration risk and price volatility.

What are the future opportunities in the Indium Based Metal Chemicals market?

Major opportunities include IGZO adoption in advanced displays, InP use in photonics and quantum technologies, CIGS thin-film solar growth, indium recycling from display scrap, and circular economy supply models. Improved recovery infrastructure could reduce supply risk and support sustainable market expansion.

Competitive Landscape:

The global indium based metal chemicals market is moderately consolidated, characterized by a mix of large vertically integrated producers and specialized high-purity chemical manufacturers. Competitive strength is linked to feedstock access, purification capability, recycling infrastructure, quality consistency, application-specific product development, and long-term relationships with major electronics and semiconductor customers.

The top three companies—Korea Zinc (South Korea), Dowa Holdings (Japan), and Umicore (Belgium)—collectively command a significant portion of the global market as of 2025. Their strength comes from vertically integrated operations, advanced refining capabilities, high-purity production expertise, and long-standing relationships with display and electronics manufacturers.

Asahi Holdings and YoungPoong add further Japanese and Korean manufacturing depth, while Teck Resources contributes meaningful indium production linked to zinc smelting operations. Emerging Chinese producers, including Zhuzhou Smelter Group and China Germanium, are expanding production capacity to serve domestic electronics and semiconductor demand.

Specialized producers such as PPM Pure Metals GmbH in Germany occupy defensible positions in ultra-high-purity niches for research, semiconductor, and advanced materials applications. These high-value segments require impurity tolerances measured in parts per billion, creating strong barriers to entry.

List of Key Indium Based Metal Chemicals Companies Profiled:

● Korea Zinc (South Korea)

● Dowa Holdings (Japan)

● Asahi Holdings (Japan)

● Teck Resources (Canada)

● Umicore (Belgium)

● Nyrstar (Switzerland)

● YoungPoong (South Korea)

● PPM Pure Metals GmbH (Germany)

● Zhuzhou Smelter Group (China)

● China Germanium (China)

The competitive strategy across the industry is focused on advancing purification technology, improving production efficiency, expanding recycling capabilities, and forming long-term supply agreements with major end-users.

Companies are also investing in application-specific development for display technologies, semiconductors, photonics, CIGS photovoltaics, and advanced electronics. As demand shifts toward higher-purity and more complex indium compounds, suppliers with strong R&D and technical support capabilities are expected to gain market advantage.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific:

Asia-Pacific is the dominant force in the global Indium Based Metal Chemicals market, holding approximately 68% of global market share. China alone accounts for around 42% of global demand, reflecting its strong position in display manufacturing, consumer electronics, semiconductor fabrication, and zinc refining.

China’s strength in zinc refining provides a structural feedstock advantage for domestic indium chemical producers. The country also has strong demand from electronics, ITO manufacturing, solar technologies, and advanced materials.

Japan and South Korea contribute advanced technological capabilities. Companies such as Dowa, Asahi, and Korea Zinc are global benchmark producers of high-purity indium compounds. South Korea’s major display manufacturing ecosystem creates stable demand for ITO sputtering targets, while Japan’s electronics and optoelectronics industries consume Indium Phosphide and specialty compounds.

Asia-Pacific’s growing investment in renewable energy infrastructure is also supporting CIGS photovoltaic demand. The region’s integrated supply chain makes it the center of global indium chemical production and consumption.

● North America:

North America maintains a strategically important position in the Indium Based Metal Chemicals market, with demand growing at approximately 6.8% CAGR. Regional demand is driven by defense, aerospace, advanced electronics, photonics, quantum computing, semiconductor research, and critical materials initiatives.

The United States has historically been a major consumer of high-purity indium compounds used in infrared detector arrays, night-vision systems, military-grade optoelectronics, and aerospace sensors. Indium Antimonide plays a key role in many of these specialized applications.

Growing interest in quantum computing, photonic devices, and advanced semiconductor technologies is creating new demand for Indium Phosphide in research institutions and technology companies.

Canada contributes to regional production through zinc smelting operations and related indium recovery potential. The United States is also developing stronger capabilities in indium recovery and recycling as part of strategic critical materials programs.

● Europe:

Europe’s Indium Based Metal Chemicals market is characterized by advanced material science capabilities, strong sustainability focus, and specialized chemical manufacturing expertise. Germany leads the region in high-performance indium compound production for automotive electronics, industrial sensors, advanced coatings, and specialty applications.

Umicore, headquartered in Belgium, is a global leader in indium recovery from end-of-life electronics and ITO manufacturing scrap. This positions Europe strongly in the circular economy transition for critical materials.

European regulations are encouraging closed-loop recycling frameworks and improving secondary indium recovery rates. Current regional recovery rates stand at approximately 35%, ahead of the global average.

Europe’s combination of production expertise, recycling capability, and regulatory alignment creates a strong foundation for future growth. The region is especially well positioned in sustainable indium sourcing, high-purity specialty chemicals, and advanced electronics applications.

● South America, Middle East & Africa:

South America, the Middle East, and Africa represent emerging frontiers for the Indium Based Metal Chemicals market. While current demand remains modest, these regions hold long-term potential through zinc mining, industrial development, electronics manufacturing, renewable energy, and downstream chemical processing.

South America has untapped indium resource potential linked to substantial zinc mining bases in countries such as Peru and Bolivia. Brazil is gradually developing domestic electronics manufacturing capabilities, which could support future downstream demand for indium chemicals.

The Middle East, particularly the UAE and Saudi Arabia, is investing in electronics manufacturing, renewable energy infrastructure, and industrial diversification. These trends may gradually create demand for indium-based materials used in displays, photovoltaics, and advanced electronics.

South Africa’s established zinc mining sector offers future potential for indium byproduct recovery. However, downstream chemical processing capabilities in the region remain at an early stage.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307153/indium-based-metal-chemicals-market

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307153/indium-based-metal-chemicals-market

Need More In-Depth Market Intelligence?

The complete report provides detailed insights into:

✔ Regional demand forecasts

✔ Production capacity analysis

✔ Pricing trends

✔ Competitive landscape

✔ Supply chain developments

✔ Emerging opportunities

✔ Product type analysis

✔ Application-wise growth outlook

✔ Recycling and circular economy trends

Access the Full Report:

https://www.24chemicalresearch.com/reports/307153/indium-based-metal-chemicals-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a trusted provider of chemical market intelligence, serving clients including over 30 Fortune 500 companies. The company provides data-driven insights through rigorous research methodologies, helping businesses understand government policy, emerging technologies, competitive landscapes, production capacity, pricing movements, and supply chain developments.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030